The Metric That Settles the Cat A+ Debate

Why NER, NPV, and NOI can all give you three different answers to the same question

Net Effective Rent (NER) is usually the first number anyone reaches for.

It’s the reflex move when comparing leasing strategies:

Run the NER, see which option looks better, move on.

And it works well enough when you’re comparing two incentive packages on the same lease length.

But as an owner, when deciding between traditional leasing and a Cat A+ buildout program, the standard metrics can mislead you.

The math may not be wrong, but each output is missing something different.

Two compelling strategies, one broken comparison

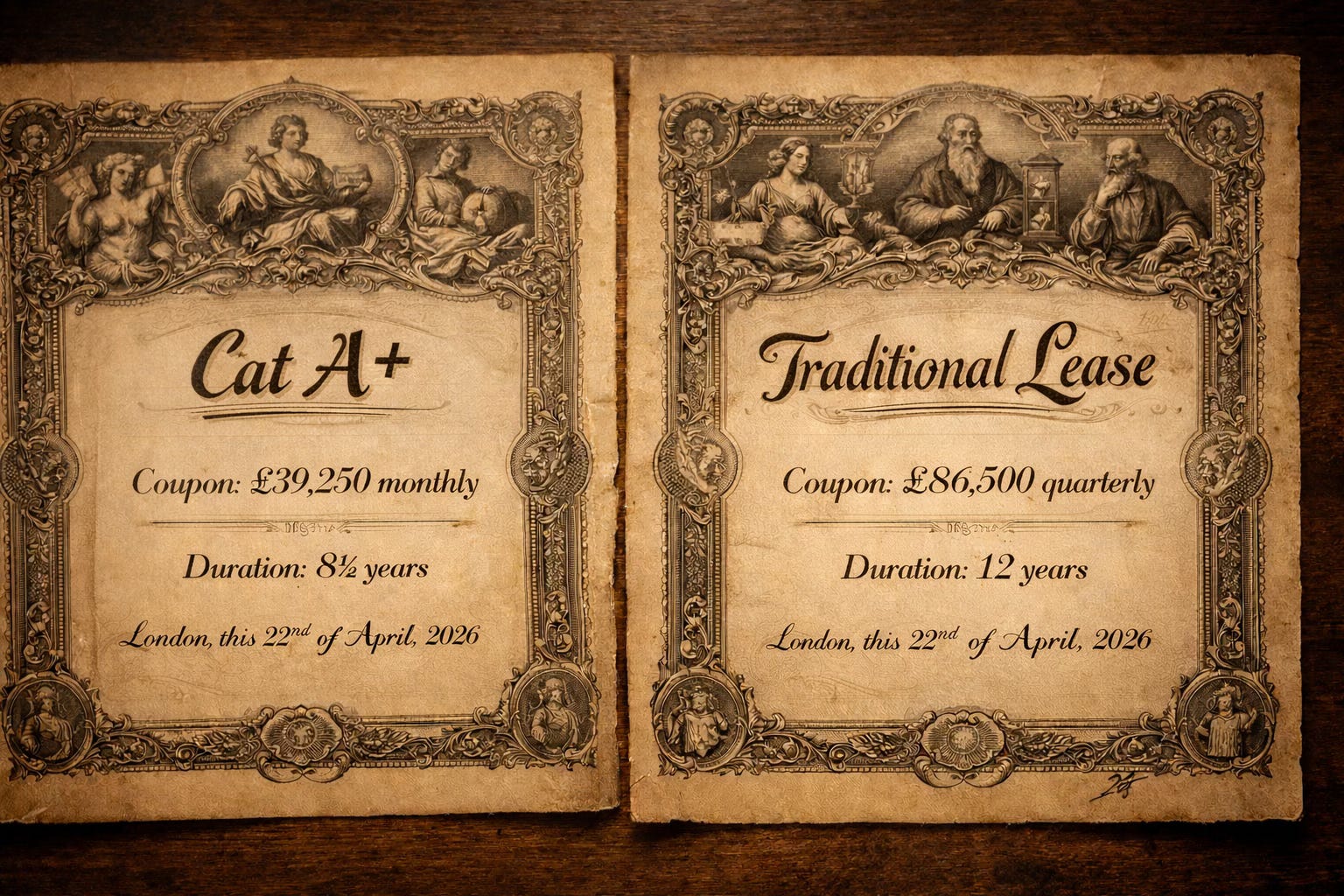

The case for Cat A+ is real:

Invest capital upfront, offer space that’s ready to occupy, and compress vacancy from months to weeks.

Tenants pay a premium for speed and certainty.

Leasing velocity improves, and carrying costs fall.

The case for traditional leasing is equally strong:

Longer leases, fewer turnover events, lower operational overhead, simpler asset management. And it carries a third advantage that rarely makes it into the NER comparison.

Valuers and lenders tend to treat it better.

A longer WAULT, a more predictable income stream, a simpler story at refinancing and exit. That has real value, even if it doesn’t show up in the headline rent.

Both strategies make money.

In a rising market, you can defend either one after the fact.

That’s part of what makes this comparison so difficult,

and so easy to get wrong without realising it.

Asking the right question with the wrong tool

Think of each leasing strategy as a bond.

You deploy capital, you receive a stream of income, and eventually the instrument matures and you make a new decision.

The question is:

Which bond offers the better return?

Not which one has more cash flows, or a higher coupon on paper,

but what it actually yields relative to what it costs.

Standard metrics each fail to answer that question in their own way.

NER is like comparing bonds by their stated coupon while ignoring the price you paid. It averages incentives across the lease term without accounting for your cost of capital. The number looks like a yield, but it isn’t one.

Net Operating Income (NOI) is closer to counting total coupon payments over the life of the bond without accounting for what you paid for it. More payments sounds better, but if the capital required to generate those payments was higher, the comparison is no longer honest. Cat A+ buildout costs typically sit below the NOI line, which can make that strategy look more attractive than it actually is.

Net Present Value (NPV) gets the cost of capital right, but penalises shorter instruments simply by having fewer cash flows to discount. A 10-year traditional lease will almost always produce a higher NPV than a Cat A+ cycle, not because it performs better, but because it runs longer. You can make traditional leasing win on NPV almost by definition. It’s the same mistake as rejecting a 7-year bond because a 10-year one exists.

Each metric can point you in a different direction.

That’s the problem.

The winner’s curse

Here’s what makes this uncomfortable:

Both strategies will likely generate positive returns.

That means whichever one you chose, you can probably defend it afterwards.

The model supported it.

The returns came in.

Case closed.

But that’s not the same as making a good decision.

If your metric pointed to Cat A+ and Cat A+ performed well, did you generate alpha?

Or did you just avoid being obviously wrong in a market that rewarded both options?

In asset management, the standard is higher than that.

You’re being paid to find the right answer, not to land on it by accident.

In a competitive market, the teams that price these decisions correctly know which assets reward a Cat A+ strategy and which ones don’t, and they bid accordingly.

That means they’ll outbid you for the assets you should want, and you’ll end up winning the ones you shouldn’t.

You won the auction.

Congratulations.

But in real estate, overpaying in an auction is just a slow way to lose.

In a rising market, this is easy to miss.

Assets appreciate, strategies look vindicated, LPs earn a return.

But as markets tighten, ‘we made money’ stops being a sufficient answer,

and it becomes very hard to explain why your competitors made more.

A better way to think about it

What you need is the equivalent of bond yield:

A single number that captures what each strategy actually returns per month, net of everything it costs to run, across its complete life.

That’s what Equivalent Monthly Annuity (EMA) does.

EMA converts every cash flow across each strategy’s full cycle into a single comparable monthly figure. Rent, free rent, commissions, vacancy, CapEx, suite refreshes — everything from initial buildout to the next major reinvestment decision. One number per strategy. Directly comparable, regardless of how long each cycle runs.

The term difference stops being an objection. Just as you’d compare a 7-year and a 10-year bond by their yield and reinvest at maturity, EMA lets you compare a Cat A+ cycle and a traditional lease on equal footing and make a new decision when each one matures.

The duration is already in the calculation.

The conversation this unlocks

Once the financial baseline is settled, the real questions can surface.

Which strategy fits the business plan:

Steady long-term income, or a more active management model with higher turnover? How will each approach be valued at exit? And does your strategy match what a buyer will underwrite?

How will lenders treat the income?

Because a portfolio of short, rolling Cat A+ tenancies looks different to a funder than a building anchored by 10-year leases, and that affects your refinancing options as much as your cap rate.

Those are the conversations worth having.

The Cat A+ debate is not settled by who can tell the best story, it’s settled by who measures the full economic reality most accurately.

If you want to pressure-test your leasing strategy with a like-for-like financial comparison across the full life of the asset, I’d love to have a chat.

This finance thought leadership article is brought to you by

ReturnSuite’s advisory service handles the financial comparison for complex leasing strategy decisions — every cash flow over the full economic life, normalised into a single defensible number.