The Flex Divide: Regional Realities in a Brave Economy

Part 3 of 4 · Q3 Rubberdesk Report: Flex Is the Backbone of the Brave Economy

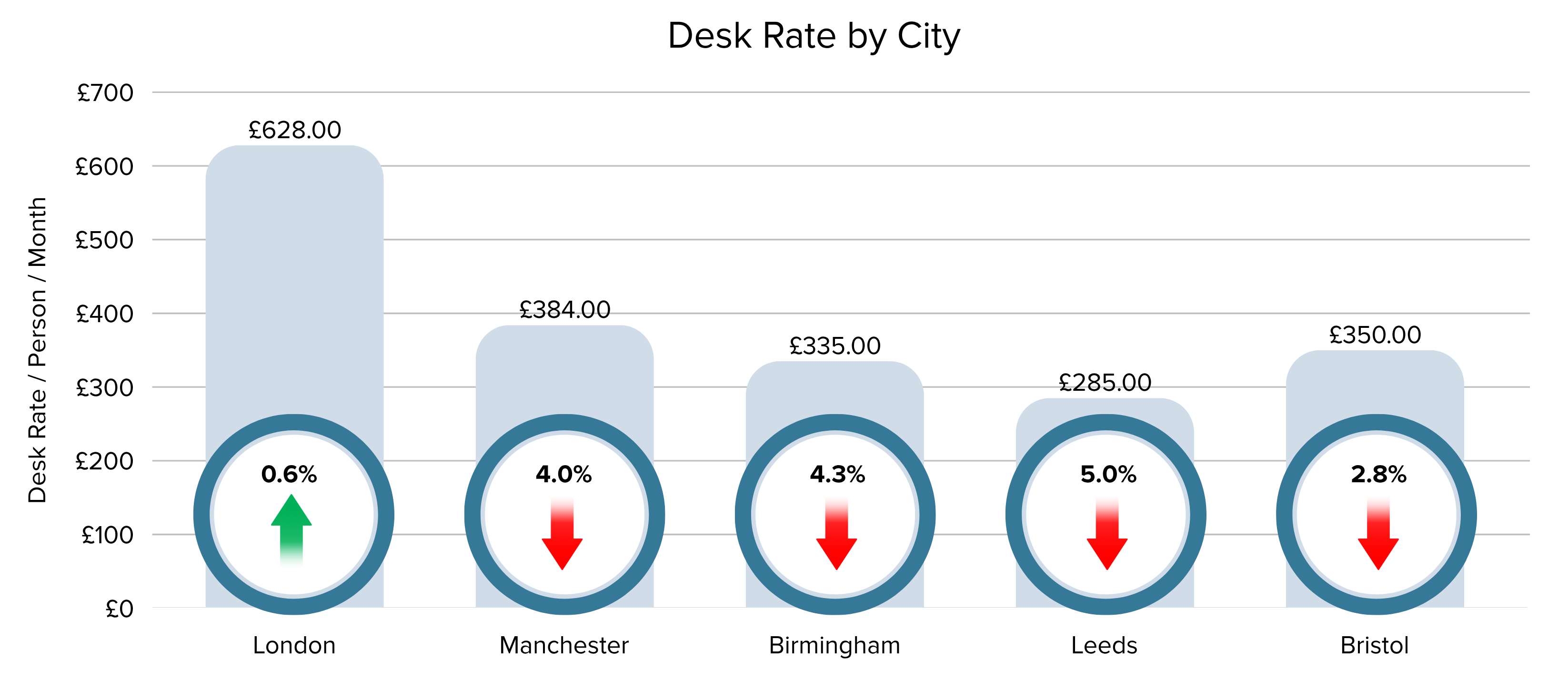

In our first article, we looked at how businesses are embracing flexibility to navigate uncertainty and, in turn, creating what we call the brave economy. But resilience does not look the same everywhere. Across the UK, flex space trends vary massively, and these trends can be used to give us insight, reflecting local confidence and strategy.

So, let us …

| A guest post by

|